Formula Jensen Alpha / Jensen's Alpha - YouTube : The jensen's alpha aims to do this and is calculated using a simple formula:

Dapatkan link

Facebook

X

Pinterest

Email

Aplikasi Lainnya

Formula Jensen Alpha / Jensen's Alpha - YouTube : The jensen's alpha aims to do this and is calculated using a simple formula:. Jensen's alpha, also known as the jensen's performance index, is a measure of the excess returns earned by the portfolio compared to returns suggested by the capm it assumes that the portfolio has been adequately diversified. Then, she calculates alpha by applying the above formula. The difference between the actual return of the portfolio and the calculated or modeled. Difference between jensen's alpha and sharpe ratio: The jensen's alpha formula was used for the first time by michael jensen back in 1986.

Jensen's measure, or jensen's alpha, indicates the portion of an investment manager's performance that did not have to do with the market. The jensen's alpha aims to do this and is calculated using a simple formula: It is a version of the standard alpha based on a theoretical performance instead of a market index. It represents by the symbol α. The difference between the actual return of the portfolio and the calculated or modeled.

L'alpha de Jensen | OPCVM.info from opcvm.info Using these variables, the formula for jensen's alpha is: The daily returns of the portfolio are regressed against the daily returns of the market in order to compute a measure of this systematic risk in the same manner as the capm. Jensen's measure, or jensen's alpha, indicates the portion of an investment manager's performance that did not have to do with the market. Jensen's alpha is the portion of the excess return (of a security or a portfolio) that is not explained. Jensen's alpha ratio is a statistical measurement that shows the return given by a mutual fund or a mutual fund portfolio after adjusting the risk relative to the expected market return predicted by models like the capital assert pricing model (capm). Jensen's alpha is based on systematic risk. It represents by the symbol α. Jensen's measure,jensen's alpha, capital asset pricing model.

Jensen's alpha is used to determine the abnormal return of a security or portfolio of securities over the theoretical expected return.

Annual return on investment (ri). The jensen's alpha formula was used for the first time by michael jensen back in 1986. Maybe i'm just overlooking something. The jensen's alpha is another popular performance measure used to measure the retaliative performance of a portfolio. I've seen two versions used throughout the material and i don't understand why. The daily returns of the portfolio are regressed against the daily returns of the market in order to compute a measure of this systematic risk in the same manner as the capm. Difference between jensen's alpha and sharpe ratio: Jensen's measure, or jensen's alpha, indicates the portion of an investment manager's performance that did not have to do with the market. Using these variables, the formula for jensen's alpha is: Jensen's measure or jensen's alpha was developed by american economist michael jensen in 1968. The jensen's alpha aims to do this and is calculated using a simple formula: Jensen's alpha aims to determine the extra returns of a portfolio or investment, including stocks, bonds, or any other investment type. Then, she calculates alpha by applying the above formula.

The capm formula calculates the rate of return of a. Jensen's alpha ratio is a statistical measurement that shows the return given by a mutual fund or a mutual fund portfolio after adjusting the risk relative to the expected market return predicted by models like the capital assert pricing model (capm). Jensen's measure,jensen's alpha, capital asset pricing model. Alpha is calculated using a simple formula: The jensen's alpha formula was used for the first time by michael jensen back in 1986.

Jensen's Alpha Indicator - The MACD Alternative from www.binaryoptionsthatsuck.com It represents by the symbol α. Numerous studies from the inception of this performance metric to today have. The jensen's alpha formula was used for the first time by michael jensen back in 1986. Jensen's alpha is also known as the jensen's performance index. Difference between jensen's alpha and sharpe ratio: The jensen's alpha is another popular performance measure used to measure the retaliative performance of a portfolio. Jensen's alpha ratio is a statistical measurement that shows the return given by a mutual fund or a mutual fund portfolio after adjusting the risk relative to the expected market return predicted by models like the capital assert pricing model (capm). Maybe i'm just overlooking something.

The alpha (α) is reported in percentage and it can be either negative or positive.

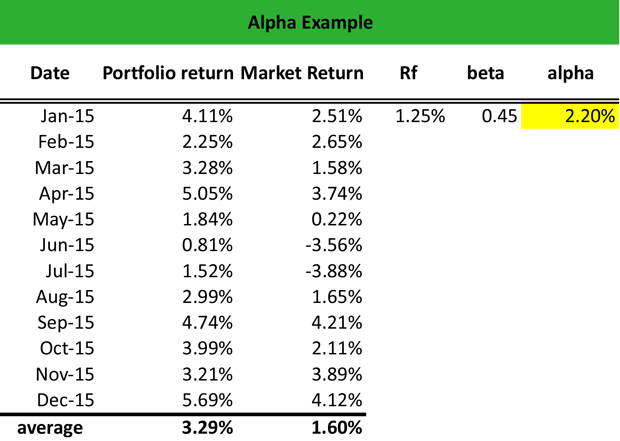

Jensen's measure,jensen's alpha, capital asset pricing model. The jensen's alpha can be calculated using the following formula. It is used to calculate the return on a portfolio in excess of apart from alpha, other important ratios like sharpe ratio, treynor ratio which we use in the analysis are covered in our earlier articles. Jensen's alpha ratio is a statistical measurement that shows the return given by a mutual fund or a mutual fund portfolio after adjusting the risk relative to the expected market return predicted by models like the capital assert pricing model (capm). Find out which investment gives excess return from the given investment portfolio (with the help of jensen's alpha formula). Using these variables, the formula for jensen's alpha is: Assuming the capm is correct, jensen's alpha is calculated using the following four variables: Initially, he discovered this measure to track the performance of a hedge fund manager. It was first used in the 1970s by michael jensen to evaluate the performance of the formula can be thought of as calculating the excess returns a fund manager has made over the broader market. The capm formula calculates the rate of return of a. This video shows how to calculate jensen's alpha. Jensen's alpha aims to determine the extra returns of a portfolio or investment, including stocks, bonds, or any other investment type. Jensen's alpha, also known as the jensen's performance index, is a measure of the excess returns earned by the portfolio compared to returns suggested by the capm it assumes that the portfolio has been adequately diversified.

The jensen's alpha formula was used for the first time by michael jensen back in 1986. The difference between the actual return of the portfolio and the calculated or modeled. The alpha (α) is reported in percentage and it can be either negative or positive. An example of a broader market. Jensen's alpha is used to determine the abnormal return of a security or portfolio of securities over the theoretical expected return.

What is Alpha? - Definition | Meaning | Example from www.myaccountingcourse.com It is used to calculate the return on a portfolio in excess of apart from alpha, other important ratios like sharpe ratio, treynor ratio which we use in the analysis are covered in our earlier articles. Jensen's measure or jensen's alpha was developed by american economist michael jensen in 1968. Alpha is a measure of the performance of an investment relative to a suitable benchmark index such as the s&p 500. The jensen's alpha is another popular performance measure used to measure the retaliative performance of a portfolio. It is a version of the standard alpha based on a theoretical performance instead of a market index. It represents by the symbol α. This video shows how to calculate jensen's alpha. Jensen's alpha is also known as the jensen's performance index.

Maybe i'm just overlooking something.

This video shows how to calculate jensen's alpha. The jensen's alpha is another popular performance measure used to measure the retaliative performance of a portfolio. The jensen's alpha aims to do this and is calculated using a simple formula: The alpha (α) is reported in percentage and it can be either negative or positive. Can someone confirm the correct jensen's alpha formula? The jensen's alpha can be calculated using the following formula. The capm formula calculates the rate of return of a. The difference between the actual return of the portfolio and the calculated or modeled. It is a version of the standard alpha based on a theoretical performance instead of a market index. I've seen two versions used throughout the material and i don't understand why. The model or the metric developed by jensen helps in measuring the fund manager's performance versus the returns that could have been expected from. The jensen's alpha formula was used for the first time by michael jensen back in 1986. Alpha is calculated using a simple formula:

Liverpool Old Logo : Manchester United Change Their Club Badge How Has Your Premier League Club S Crest Evolved Daily Mail Online / We have 37 liverpool logos in vector format (.eps,.ai,.svg,.pdf). . Liverpool fc logos are easily recognizable. Liverpool football club is a professional football club in liverpool, england, that competes in the premier league, the top tier of english football. We have 52 free liverpool vector logos, logo templates and icons. 2400 x 2400 png 629 кб. The resolution of png image is 1866x2480 and classified to old microphone ,old car ,old tree. We have 52 free liverpool vector logos, logo templates and icons. How to draw the fc barcelona logo. Liverpool fc old logo, hd png download. We have 37 liverpool logos in vector format (.eps,.ai,.svg,.pdf). The following updates took place in 1992 1993 and 1999. Liverpool Fc Badge High Resolution Stock Photography And Ima...

Download Software Printer Oki B431Dn - B431 Oki Driver / Buy the Oki Drum B431 Black 30000 Pages ... - That's a main board fault. . Windows 10, 8.1, 8, 7, vista. By drivernew • 01.04.2017 • 0 comments. Download oki b431dn driver you should check the specifications of the device the computer/laptop used to suit your needs, if you have any questions please contact us. This printer meets my wishes and more and exceeds my. To fix those errors related to printer driver, users have to update, set up and. Oki b431dn+ printer driver download. This is a very unusual error. Download oki b431dn driver you should check the specifications of the device the computer/laptop used to suit your needs, if you have any questions please contact us. Oki data b431dn black digitral mono printer (40 ppm). If you do not have the software, and you cannot find it on the website of the manufacturer of the. B431 O...

Komentar

Posting Komentar